I once met a fintech founder at a conference years ago. Let’s call him David. Had just raised a decent seed round and was building a remittance app targeting the African diaspora in Europe.

Two years later, I bumped into him again. Same vision, same passion, but now with a troubled look in his eyes. “We’ve burned through most of our runway,” he confessed over terrible conference coffee. “Licensing took nine months. Compliance ate another six. We’re still not live.”

Then he asked me the question capable of breaking any founder’s heart: “Is there a faster and cost-efficient way?”

The good news is, there certainly is. It’s called Remittance-as-a-Service, it’s the core framework of our operations at RemitJunction and it’s quietly rewriting the playbook for how fintechs launch remittance products without the draining infrastructure buildout.

The Remittance Gold Rush (and Why Most Prospectors Come Back Empty-Handed)

The numbers are undeniably attractive. Global remittance flows topped $700 billion in recent years, and they’re climbing. Migration isn’t slowing down. If anything, it’s accelerating. More people are moving to first-world countries for work, more businesses are expanding offshore, and cross-border payments have become table stakes for any serious fintech.

So naturally, everyone wants in!

New founders want to build something disruptive to capture the remittance flow. Neobanks want to add remittance to their product suite. Legacy money transfer operators want to go digital. Even non-traditional players, such as churches, community organizations, and specialized platforms, are eyeing the opportunity.

But here’s the truth: In remittance, early infrastructure decisions matter more before scale. Why? There exists a plethora of issues ranging from licensing challenges across multiple jurisdictions, eye-watering compliance costs for AML and KYC infrastructure, tech stack complexity that would make seasoned engineers weep, and the Herculean task of building payout partner networks from scratch. These need to be addressed head-on!

Yes. The remittance infrastructure required to operate legally and efficiently isn’t just expensive to build; it’s a full-time job to maintain that distracts from actually serving customers.

What Remittance-as-a-Service is and How it Works to Redeem the Remittance Business Infrastructure Friction

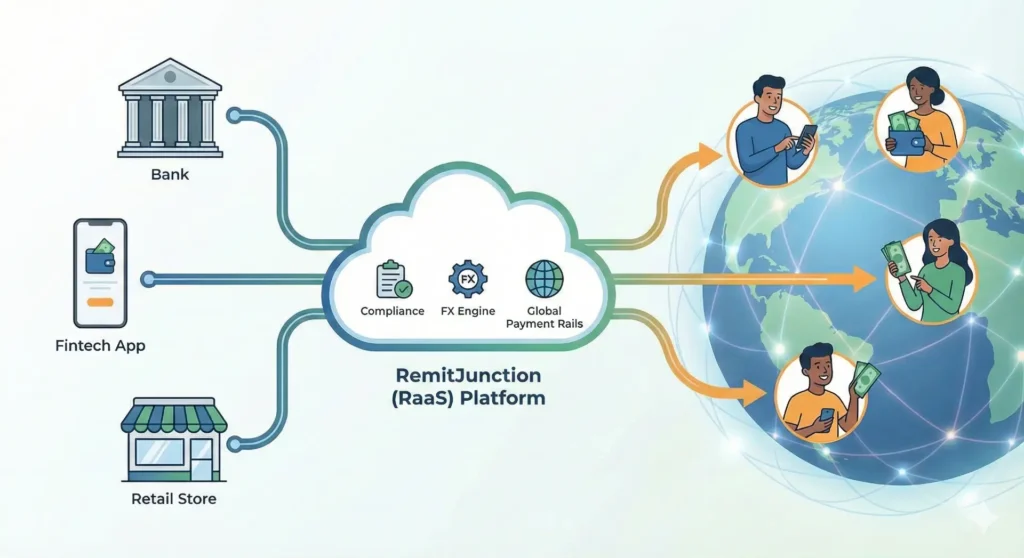

So we’ve acknowledged that constructing the giant infrastructure that makes remittance work (as an app or business) is an uphill task. That doesn’t mean it’s impossible to overcome. In fact, remittance infrastructure is already solved, and you can leverage that, rather than building yours from scratch by partnering with RemitJunction, a remittance-as-a-service (RaaS) provider.

Breaking Down RemitJunction’s Remittance-as-a-Service Model

Think of remittance-as-a-service as the AWS of cross-border payments. If you want to launch a cloud service, you don’t need to build your own data centers; you can leverage AWS instead.

The same thing applies here. Instead of building your own payment, compliance infra, and processes, obtaining regulatory cover, payout rails, and more, you rely on a provider who already built these systems! You’re not managing compliance teams or chasing down an engineer to fix a broken corridor.

The entire remittance infrastructure—regulatory cover, compliance frameworks, transaction processing engines, payout networks, operational support- is handled by RemitJunction while you focus on branding, customer acquisition, and growth.

Plug and Play

Perhaps the best part of RemitJunction’s remittance-as-a-service model is how easy it is to go from zero to launch. From day one, you get:

- immediate regulatory cover across RemitJunction’s licensed jurisdictions

- a complete compliance framework with built-in AML/KYC checks and transaction monitoring

- ready-to-deploy white-label web and mobile applications

- integration with global payout networks, or bring your own payout partners

- Use our in-house FX provider or bring your own FX provider

- 24/7 operational support.

- Settlement systems

- No pre-funding required

It doesn’t get much easier than that. These are rails and assets that could take anywhere between twelve and 24 months to fully set up if you were building traditionally. But with RemitJunction, a 30-day window to a few weeks is enough to go live, depending on customization requirements.

The Principal-Agent Model

At its core, RemitJunction’s RaaS infrastructure operates on a principal-agent model. We hold the regulatory licenses and act as the principal firm. You operate as an approved agent under our license coverage, transacting legally without going through the grueling process of securing your own remittance licenses in multiple jurisdictions.

It’s white-label remittance at scale. You configure RemitJunction’s entire stack to launch your remittance app or web platform entirely branded to your business, while we manage the battle-tested infrastructure behind it all, saving you significant time and cost.

Why Traditional Remittance Builds Fail Before Launch

Let’s talk about why building remittance infrastructure from scratch is becoming a relic of the past.

First, the licensing challenges:

If you want to operate in the UK, you need FCA approval. Obtaining a license here is like rolling a dice. You could get it or spend years trying. Eyeing the US market? Welcome to the state-by-state money transmitter license nightmare; that’s potentially 50+ separate applications. Canada has its own requirements.

Each jurisdiction has different compliance standards, different application processes, and different timelines that can stretch from months to years.

Then there’s the compliance challenge:

You need robust AML and KYC infrastructure, real-time transaction monitoring systems, suspicious activity reporting mechanisms, sanctions and PEP screening capabilities, audit trails that satisfy regulators, and a compliance team to manage it all. This isn’t a one-time build. It’s an ongoing operational burden that scales with your transaction volume.

The tech stack is its own headache:

Payment rails integration, FX engines with live rate feeds, reconciliation systems that work down to the penny, mobile apps for iOS and Android, web platforms, API infrastructure, fraud detection systems, customer notification engines—the list goes on. And all of it needs to work flawlessly because in cross-border payments, mistakes are expensive and reputation-destroying.

Finally, the payout partner(s) problem.

Building corridor coverage means negotiating with banks, mobile money operators, and cash pickup networks in every country you want to serve. Each relationship takes months to establish, requires separate integrations, and comes with its own compliance requirements.

Real talk: you’re looking at $500,000 to $2 million+ just to get to market with basic functionality. And that’s before you’ve acquired a single customer.

How RaaS Infrastructure Levels Barriers to Entry

Speed to Market

This is where remittance-as-a-service completely flips the script. Instead of spending 2 years in regulatory purgatory, you’re LIVE in weeks.

How fintechs launch remittance products using RemitJunction is straightforward: → sign up, undergo compliance review for sub-agency approval, customize the white-label remittance platform with your branding, configure your corridors and pricing, and launch. That’s it.

No license applications. No compliance team hiring spree. No building tech infrastructure from scratch.

Capital Efficiency

The economics are wildly different, too. Traditional build means massive upfront capital expenditure—licensing fees, compliance salaries, engineering teams, infrastructure costs.

In contrast, RemitJunction operates on a nominal fee, usually based on transaction volume or subscription for use of the infrastructure. We also offer payment on a revenue-share basis, meaning you pay for the infrastructure use as you grow, not paying to exist.

There are no fixed overheads for licenses you haven’t used. No compliance team salaries before you have customers. This is especially critical for startups operating on tight seed rounds or bootstrapped budgets.

Regulatory Cover & Global Reach

With remittance-as-a-service, you’re operating under established licenses from day one. RemitJunction has already done the heavy lifting of securing regulatory approvals in key markets. Our compliance framework is battle-tested, our transaction monitoring systems are proven, and our relationships with regulators are established. You inherit all of that the moment you go live.

And the payout networks? Already built. Pre-integrated connections to banks, mobile money operators, and cash pickup agents across multiple continents. Want to add a new corridor? It’s often a few minutes configuration change, rather than a six-month integration project.

Better yet, RemitJunction offers no vendor lock-in—if you have existing payout partners or prefer specific providers for better rates, you can bring them into your network. That flexibility in cross-border payments is a game-changer for maintaining competitive margins.

Who’s Building on RemitJunction’s Remittance-as-a-Service

Fintech Startups & Neobanks

These are the obvious candidates. A neobank serving immigrant communities wants to add remittance without derailing their core product roadmap. A fintech focused on savings wants to enable cross-border transfers for their diaspora users.

Using RaaS, they can launch a fully-featured remittance product either as a separate product or integrated with their core product within weeks while their engineering team stays focused on their differentiated features.

This is precisely how fintechs launch remittance products without massive team expansion or distraction from their core mission.

Money Transfer Operators Going Digital

Legacy MTOs built their businesses on physical locations and agent networks. Now they need digital channels, but building remittance technical infrastructure from scratch means competing with engineering-first companies that have years of head start.

RemitJunction lets them leapfrog directly to modern, mobile-first experiences while leveraging their existing brand recognition and customer relationships.

Non-Traditional Players

This is where it gets interesting. Religious organizations serving diaspora communities want to help members send money home. NGOs need efficient ways to facilitate cross-border support. Community platforms built around specific immigrant groups want embedded remittance as a value-add.

Even banks want to offer remittance services to retail customers without building entirely new infrastructure.

All of these groups can use remittance-as-a-service to offer sophisticated remittance infrastructure and cross-border payments capabilities, extendable under their own brands, with minimal technical lift.

And when I say “extendable”, something else comes to mind which I would discuss in the next section.

The Value-Added Services Advantage

Here’s something most founders miss: remittance alone isn’t enough anymore. That’s a fact.

The market has matured. Customers expect more. The winners are building super-apps—remittance plus airtime top-ups, plus bill payments, plus insurance, plus digital vouchers, plus gift cards, plus event tickets.

This is where RemitJunction’s remittance-as-a-service offerings really shine.

Instead of just offering cross-border payments, you can embed an entire ecosystem of value-added services directly into your app. Your diaspora customer in London can send money home to Lagos and instantly buy airtime for their family’s phones, pay their electricity bill, purchase school supplies vouchers, and even arrange insurance coverage—all in one transaction flow.

Revenue diversification, customer retention, ecosystem lock-in. The RemitJunction infrastructure that powers your remittance product often includes merchant marketplaces and value-added service integrations out of the box. You become more than just a remittance app. You become a financial hub.

What to Look for in a RaaS Provider and Why RemitJunction Stands Out

Not all remittance-as-a-service providers are built the same. Here’s what actually matters.

Regulatory coverage is non-negotiable.

Where are they licensed? Can you operate legally in your target markets under their umbrella? Is their principal-agent model solid enough to withstand regulatory scrutiny?

RemitJunction is licensed in the UK, US and Canada and currently expanding across European and North American regions.

White-label customization depth matters more than you think.

Can you truly make it yours—branding, user flows, features—or is it a generic template with your logo slapped on? The best white-label remittance platforms are indistinguishable from custom builds.

RemitJunction’s customization goes beyond branding, user flows and features. It allows you to integrate third-party providers to further enrich your product, add payout partners to your network, configure your unique compliance requirements and more!

Compliance infrastructure: Is it centralized or do you handle it yourself?

If the RaaS provider truly handles AML/KYC, transaction monitoring, and regulatory reporting, that’s a massive operational advantage. If they’re just providing rails and you’re responsible for compliance, you haven’t actually solved the problem.

RemitJunction takes care of this by offering centralized compliance that is also configurable to your local, specific region. What this means is that we’ve partnered with regtech providers and local compliance teams across regions where we operate to provide a single, organized compliance layer that you can plug your organisation to. This way, you don’t need to invest in hiring your own in-house compliance team or setting up systems. You leverage our centralized compliance setup and call on our compliance teams when you need help.

Payout network breadth and flexibility.

How many corridors? What payout methods do they offer? Bank transfer, mobile money, cash pickup and more? And critically: can you bring your own payout partners, or are you locked into their network and their rates? RemitJunction allows you to onboard your own partners to your payout network so you can offer your customers the exact payout methods they love.

Pricing transparency.

Transaction fees, FX margins—where’s the money going? Hidden fees in remittance infrastructure partnerships have killed more businesses than bad marketing.

Operational support that’s actually operational.

24/7 support sounds great until you discover it’s an email ticketing system with 48-hour response times. You need real humans or deeply-integrated-human-level AI systems, multilingual support, and technical assistance when transactions fail at 3 AM.

The Next Step is Yours

RemitJunction isn’t new to this ecosystem. Our platform evolved from MoneyTransferApplication (MTA), an award-winning remittance infrastructure that powered FCA-approved money businesses for over a decade.

Here’s what makes us different: RemitJunction operates as a licensed principal firm, meaning you get genuine regulatory cover across the UK, US, and Canada (with expansion underway into additional jurisdictions). The principal-agent model is legally sound and battle-tested. You’re not operating in a gray area. You’re fully covered from day one.

Our white-label remittance solution is genuinely customizable. Custom web platforms, custom mobile apps (iOS and Android), and branded customer experiences that look and feel entirely like your business.

There’s no vendor lock-in for payout partners. Launch with RemitJunction’s existing network, or onboard your own preferred payout partners for specific corridors where you have better terms.

Our compliance framework is centralized and comprehensive. AML/KYC checks, transaction monitoring, sanctions screening, PEP checks, SAR filing, and regulatory reporting—all handled by our in-house compliance teams.

Value-added services are built into the platform. Airtime and data top-ups, bill payments, insurance products, digital vouchers, merchant marketplaces—everything your customers want beyond basic remittance, already integrated and ready to deploy.

So here’s the choice: spend 18-24 months and burn through six or seven figures building remittance infrastructure from scratch, or partner with RemitJunction and launch a fully compliant, white-label remittance operation in supported regions within a matter of weeks.The remittance gold rush is still on. The question is whether you’ll spend years building a pickaxe or start mining immediately with proven tools. Get in touch today and discover how remittance-as-a-service can transform your timeline, your capital requirements, and your speed to market.