Let me paint you a picture of a typical scenario that frequently occurs with funds disbursed for humanitarian purposes:

A humanitarian organization has just secured emergency funding. People on the ground need it urgently. Not in three business days. Not after the wire clears three intermediary banks and loses 4% to fees. Now!

The programme manager opens a laptop, logs into their disbursement portal, and… waits. The payment file is rejected. Wrong format. They try again.

The bank’s API is down for scheduled maintenance. Then they try a workaround. The compliance team flags it. Meanwhile, real people are waiting.

This happens frequently with institutional cross-border disbursement, whether aid, payroll, grants, or bulk transfers. It’s one of the most chronically underserved use cases in global payments. Organizations that move large volumes of money across corridors consistently run into the same wall: the infrastructure simply wasn’t built for them.

The good news is that this doesn’t have to be the case anymore. Modern technologies and designs are changing this. If you’re a bank, telco, NGO, or enterprise operating cross-border disbursements at scale, this piece is for you.

The Real Problem With Institutional Cross-Border Disbursement

Most enterprise disbursement challenges live deep in the pipelines. That is, the systems and switches that move the money from the senders to the entities.

When a telco wants to pay out commissions to agents spread across five African countries, or an NGO needs to fund hundreds of last-mile recipients in Ghana, Kenya, and Senegal simultaneously, the blockers are almost always the same: fragmented payout rails, inconsistent compliance posture across corridors, settlement timing mismatches, and the sheer operational overhead of managing multiple relationships with local partners.

Throw in the compliance question — AML, KYC, sanctions screening, SAR obligations — and you’re looking at a full-time operation before you’ve moved a single dollar. Most organizations either under-resource this and run the risk of regulatory noncompliance, or over-resource it and erode margins. Neither is a great outcome.

What institutional senders actually need is a single remittance infrastructure that handles payout diversity, centralises compliance, and gives them programmatic control over the entire disbursement lifecycle.

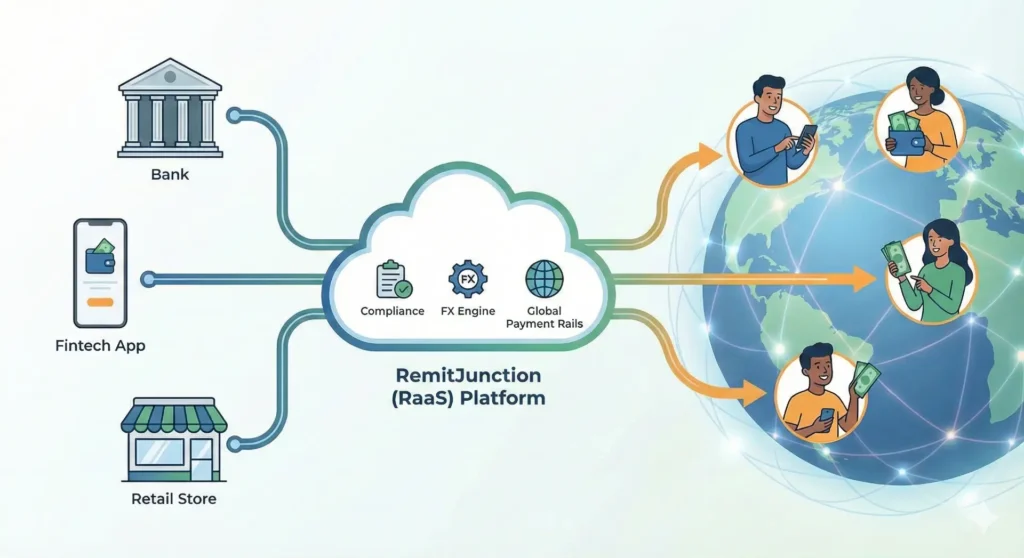

What RemitJunction Does to Solve These Problems.

If you’re evaluating a bulk payment platform for institutional disbursement, the infrastructure conversation has to cover three non-negotiables: payout coverage, compliance architecture, and API depth.

Payout Coverage That Matches Where Your Recipients Actually Are

The global South, particularly Sub-Saharan Africa, is not a single market. Nigeria has NIBSS. Kenya has M-Pesa. Ghana has GhIPSS and a thriving mobile money ecosystem. Senegal has Wave.

A bulk remittance payments platform that only supports SWIFT wires will strand a significant portion of your recipients in every single disbursement run.

RemitJunction supports bank transfers, mobile money wallets, and cash pickup agents, often within the same payout batch. This multi-rail payout capability is what separates serious infrastructure from glorified wrappers.

Centralized Compliance Across Every Corridor You Touch

Here’s where most organizations get into trouble. They build payout capability but compliance becomes a patchwork of local partners, manual processes, and well-meaning but understaffed teams trying to stay on top of 12 different regulatory environments at once. It doesn’t scale. And regulators notice.

RemitJunction’s infrastructure runs KYC, KYB, AML screening, sanctions checks, PEP screening, and transaction monitoring from a single compliance engine; not as a checklist, but as a live, automated layer embedded into every transaction.

When a disbursement triggers an anomaly flag, it’s caught, held, and reviewed without manual intervention, derailing the rest of the batch.

API Depth: Programmatic Control for Disbursement API Fintech Use Cases

For banks, telcos, and enterprises running disbursements at any meaningful volume, manual portals are a dead end. You need a disbursement API fintech solution that lets your systems talk directly to the payment infrastructure, triggering batch runs, querying transaction states, retrieving settlement data, and handling exceptions programmatically.

RemitJunction’s API goes further: it gives your finance team real-time reconciliation data, automatically matching disbursement values to settlement confirmations from payout partners.

It gives your operations team transaction-state visibility across every leg of the payment — so exceptions surface before they become complaints. And it gives your compliance team an audit trail that doesn’t require a data engineering project to query.

How RemitJunction Enables Institutional Cross-Border Disbursement

Built as an operational remittance infrastructure for regulated money businesses, RemitJunction has been processing real transactions across live corridors for over a decade, just under a different name, “MTA.”

As a licensed principal firm, RemitJunction provides regulatory cover that institutional senders need without having to acquire or maintain their own licences. Organizations onboard as appointed agents, operating cross-border payouts under RemitJunction’s regulatory framework.

This is particularly valuable for NGOs asking how NGOs send money across borders without drowning in licensing logistics, and for enterprises exploring white-label remittance platforms that let them move fast without building from the ground up.

On the payout side, RemitJunction’s network covers multiple countries with support for bank transfer, mobile money, and cash pickup — all accessible through the same integration.

For organizations running cross-border payroll solutions across Africa, this multi-rail capability means the same disbursement run can credit a bank account in Lagos, top up a mobile wallet in Accra, and route a cash pickup in Nairobi without managing three separate partner relationships.

RemitJunction’s Remittance-as-a-Service infrastructure handles the compliance layer centrally — KYC/KYB verification, AML and CFT screening, sanctions and PEP checks, automated transaction monitoring, fraud detection, and SAR filing — so institutional senders don’t have to build and maintain this apparatus independently across every corridor they operate.

The compliance engine is embedded into the payment flow, not bolted on after the fact.

For FX, RemitJunction gives disbursing organizations control over their pricing strategy: set your own FX margins, access live market rates, and manage currency conversion in real time. For organizations running large-volume disbursements where basis points matter at scale, this flexibility is operationally significant.

Organizations that don’t want to build custom front-ends can deploy RemitJunction’s fully branded interfaces.

But for enterprises and institutional senders that need deep integration with existing systems, the API-first approach lets your engineering team plug RemitJunction’s bulk remittance payments platform directly into your disbursement workflow — triggering, tracking, and reconciling at whatever volume you operate.

Who This Is Actually Built For

The use cases for institutional cross-border disbursement on RemitJunction’s bulk payment platform are broader than most people initially assume:

- NGOs and humanitarian organizations that need to disburse aid or programme funds to last-mile recipients across multiple countries — and need audit-grade documentation to satisfy donor reporting requirements.

- Telcos running agent commission payouts, airtime reseller payments, or subscriber refunds across footprint markets where the payout mix includes mobile wallets prominently.

- Banks and financial institutions that want to offer cross-border payroll solutions for Africa-facing corridors without building and licensing an independent remittance operation.

- Enterprises with distributed workforces, affiliate networks, or supplier bases in emerging markets who need reliable, compliant disbursement infrastructure without the overhead of managing it in-house.

The Smarter Way Forward for Cross-Border Disbursement

The era of stitching together five different vendor relationships to run a single disbursement corridor is, mercifully, ending.

The maturity of Remittance-as-a-Service infrastructures means that organizations of all sizes can now access enterprise-grade cross-border disbursement capability without enterprise-grade setup costs or timelines.If you’re ready to move past the patchwork and run cross-border disbursements on infrastructure built for the job, explore how RemitJunction powers UK-Africa corridors — or get in touch with the team to discuss your disbursement use case directly.